Effective management of business technology requires proactive and analytical financial steering to justify operational performance, investment feasibility and allocation of costs. Management, along with decision making, is dependent on transparency with clear structures and processes surrounding financial management.

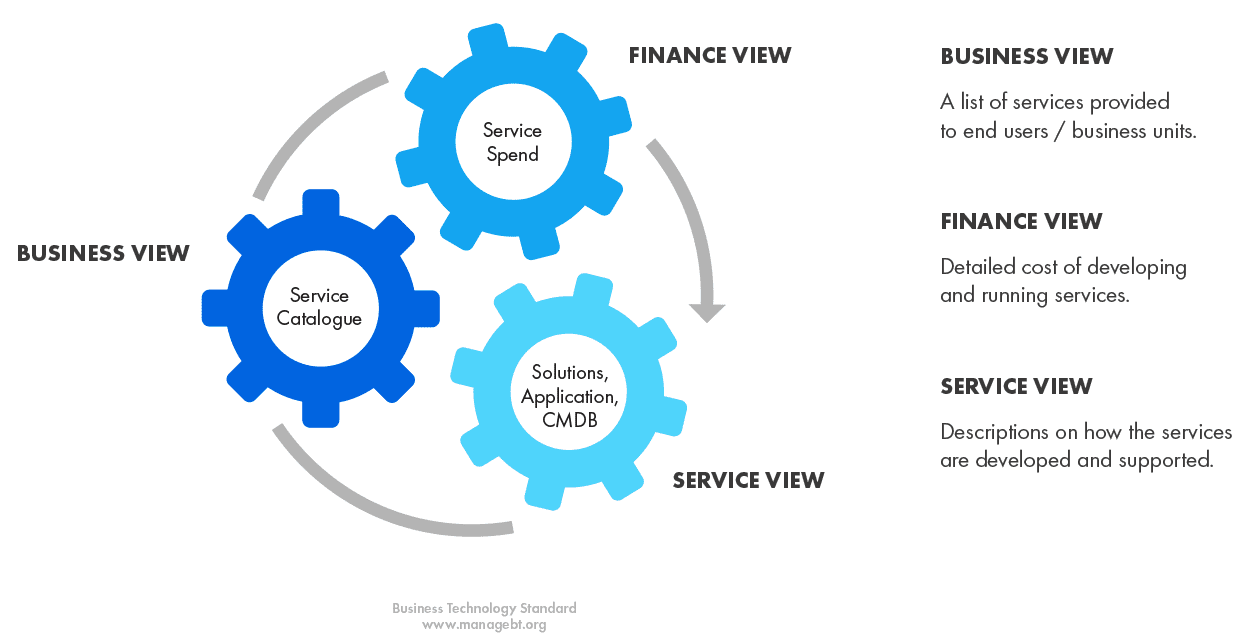

Figure 4.4.1 Financial management views

Financial transparency shows how accumulated costs are transferred to service consuming fees and how actuals correlate to plans. Financial planning ensures:

Cost transparency is not easy to achieve. Spends accumulate on general ledger level while budgeting is done on business technology element level and business is invoiced on a higher business technology services level. The best practices to tackle cost transparency are using a standardised taxonomy and grouping costs to pre-defined cost groups and services. As well as utilising a rule-based cost modelling system to automate calculations.

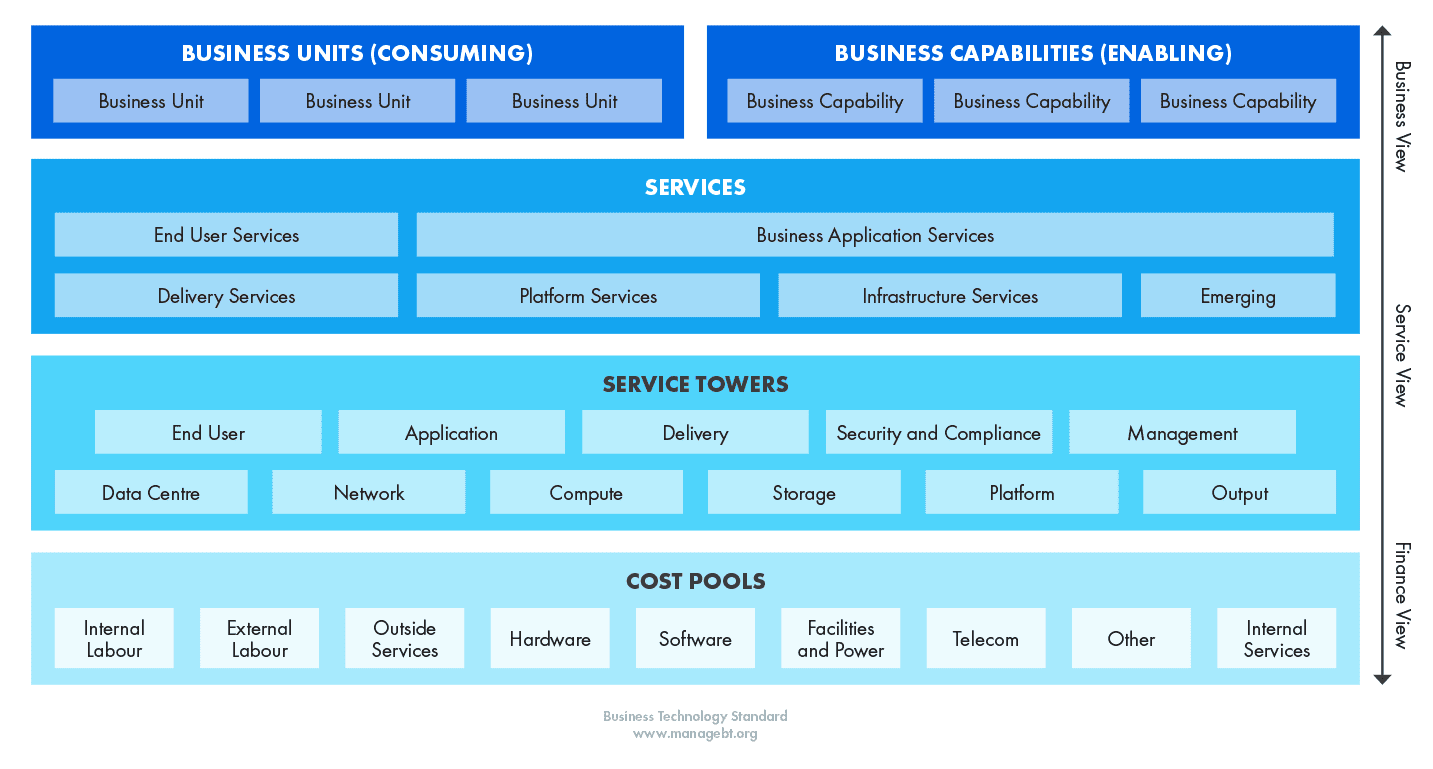

Technology Business Management (TBM) taxonomy defines standard cost sources, technologies, resources, services and capabilities to provide leaders with the facts they need to communicate the value of technology and make fact-based decisions. Standardised taxonomy also enables effective collaboration and communication between business management, business technology management and service development and delivery management. A simplified view of the taxonomy is illustrated below.

Figure 4.4.2 Technology Business Management (TBM) taxonomy

Financial feasibility provides feasibility analysis about proposed, on-going and completed development initiatives and feasibility of on-going services throughout their lifecycle by assessing:

Financial steering contributes to strategic planning and service portfolio steering by providing insights about optimal allocation of financial resources. It provides insights on:

Financial management should not be seen only as a function operated by finance. To be effective, it requires contributions and collaboration from multiple business functions, including business technology, and is enabled by using standardised models, terminology and ways of working. Transparency, accurate planning and treating financial management as a strategic capability allows businesses to create and demonstrate the value of technology.